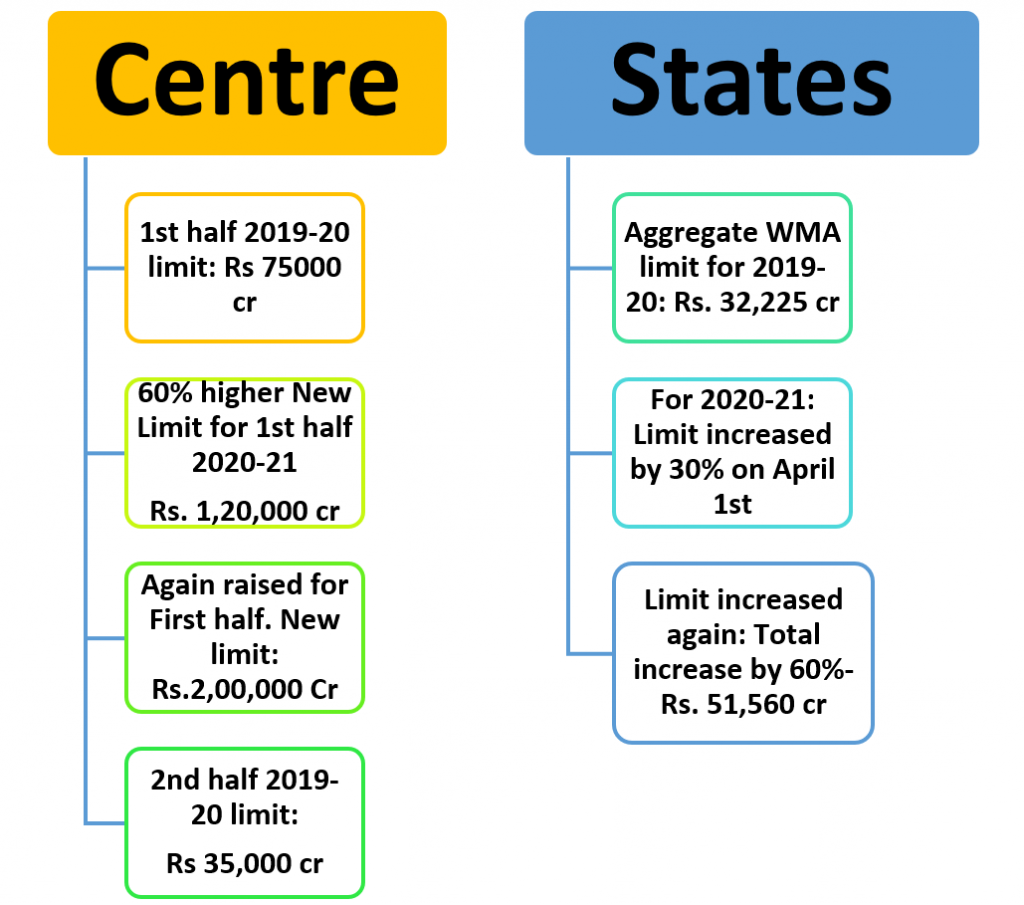

India’s Central bank recently announced an increase in the Ways and Means Advances (WMA) limits to States enabling them “to undertake COVID-19 containment and mitigation efforts” and “to better plan their market borrowings”. For the first half of FY21, WMA limit of States has been increased by 60 per cent over the level as on March 31, 2020.

What is WMA?

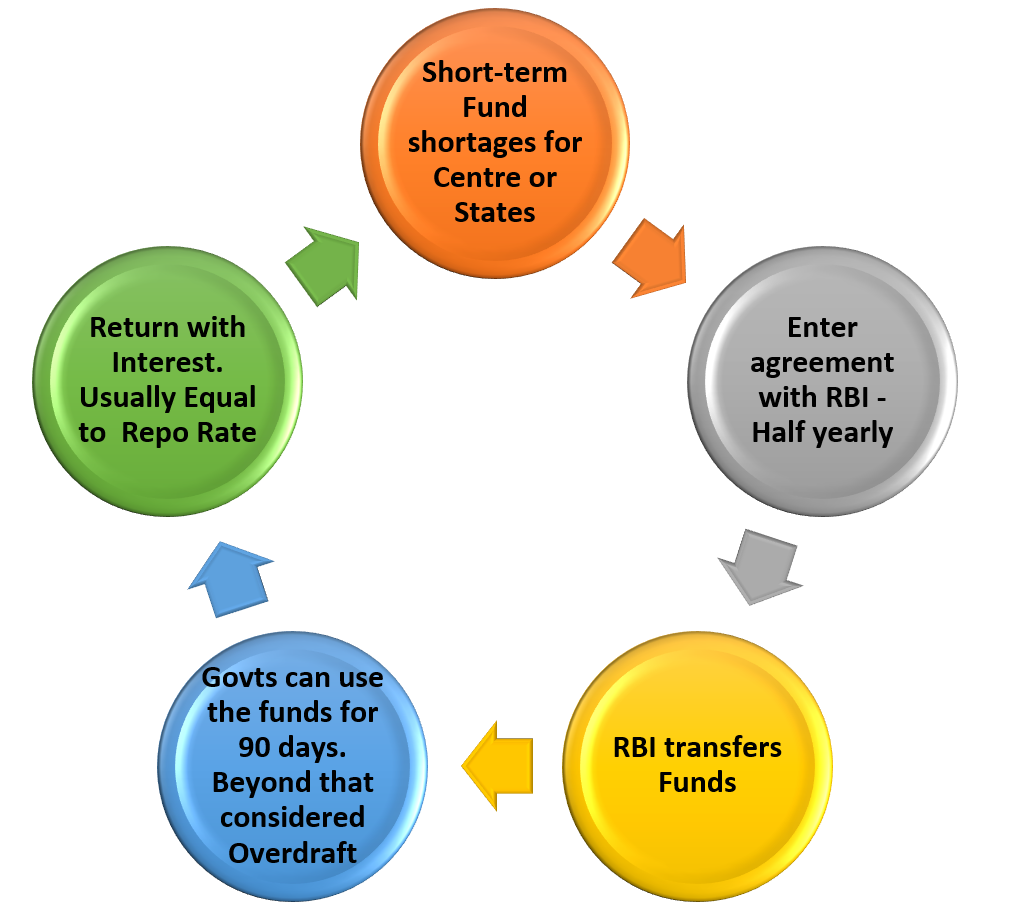

The Reserve Bank of India (RBI) gives temporary loan facilities to the central and state governments. This loan facility is called Ways and Means Advances (WMA).

When managing money, we know that cash outflows often overshoot inflows. When businesses face this, they approach banks to get working capital loans. But State governments in India either go for market borrowings by issuing securities or seek short-term funding from the RBI. Such Borrowings through WMA are to be repaid within three months and usually offered at the repo rate.

In that sense, they aren’t a source of finance per se, thus not a part of Fiscal Deficit. Section 17(5) of the RBI Act, 1934 authorises the central bank to lend to the Centre and state governments subject to their being repayable “not later than three months from the date of the making of the advance”.

When was WMA introduced?

The Ways and Means Advances scheme was introduced in 1997.

What was the Purpose of the WMA scheme?

The Ways and Means Advances scheme was introduced to meet mismatches in the receipts and payments of the government.

What is Ways and Means Advances limit?

The limits for Ways and Means Advances are decided by the government and RBI mutually and revised periodically, usually half-yearly.

There is a State-wise limit for the funds that can be availed via WMA. These limits depend on many factors, including total expenditure, revenue deficit and fiscal position of the State. WMA limits are revised periodically and the previous utilisation rates are considered while determining revised limits.

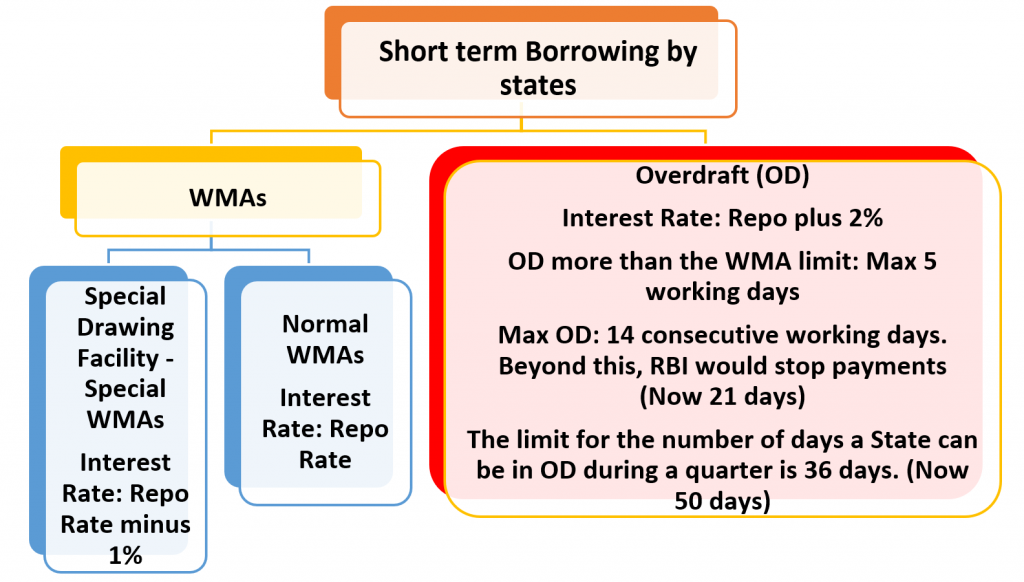

Types of WMAs and Interest rates

The interest levied for special WMAs are lower than the repo rate due to the backing of government securities.

Importance and advantages of higher Ways and Means Advances

The cash flow problems of State governments, which were already under stress, have been aggravated by the impact of Covid-19. With economic activity at a near standstill, there is hardly any money coming in from GST, petroleum products, liquor, motor vehicles, stamp duty or registration fee. As frontline fighters against Covid-19, many States are in need of immediate and large financial resources to deal with challenges, including medical testing, screening and providing income and food security to the needy.

- Increased WMA limit for States to borrow short-term funds from the RBI provides a financial cushion when there’s uncertainty in revenue collections due to stressed economic conditions.

- WMA can be an alternative to raising longer-tenure funds from the markets, issue of State government securities (State development loans) or borrowing from financial institutions for short-term funding.

- WMA funding is much cheaper than borrowings from markets.

Some states are not happy about the Ways and Means Advances Announcement

Having said that, not all States were pleased with this announcement. Some voiced concerns that increasing WMA limits would not be sufficient and demanded a moratorium on loans and interest for nine months, while others complained about the short window to repay (90 days).

Why should we care?

WMA funding can help fill the gap, though only partly. WMAs also help rein in borrowing costs of States, helping their finances in the long run. Lower borrowing costs of your State imply lower local tax collections from you

Can the Governments borrow for long-term from RBI?

Given the present condition, the Centre might have to invoke Section 5(3) of its Fiscal Responsibility and Budget Management Act, 2003. That overriding provision in the Act – which otherwise bars the RBI from lending to the government, except for meeting temporary cash flow mismatches – allows the central bank to “subscribe to the primary issues of Central Government securities” under very specified grounds. Those cover, among other things, “act of war” and “national calamity”.

Apart from monetisation of deficits – which is what this provision effectively entails – the RBI may, in the coming day, also have to undertake increased secondary market purchases and sales of Central as well as state government securities.