IMPORTANT TERMS:

| Import elasticity of exports: An analysis of the relationship between exports of finished goods and imports of raw materials and intermediate goods for India is being undertaken. Net International Investment Position (NIIP): NIIP measures the gap between a nation’s stock of foreign assets and foreigner’s stock of that nation’s assets at a specific point in time. Foreign Exchange Reserves: The FOREX is reserve assets held by a central bank in foreign currencies. It acts as a buffer to be used in challenging times and used to back liabilities on their own issued currency as well as to influence monetary policy. Components of Indian FOREX Reserves: Foreign currency assets (FCAs), Gold, Special Drawing Rights (SDRs) and RBI’s Reserve position with International Monetary Fund (IMF). FCAs constitute the largest component of Indian FOREX Reserves. External Debt: It is owed to creditors outside the country. The outsider creditors can be foreign governments, International Financial Institutions like WB, IMF, etc., corporate and foreign private households. External debt may be of several kinds such as multilateral, bilateral, IMF loans, Trade credits, External commercial borrowings, etc. |

KEY FACTS

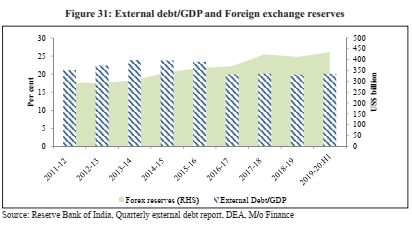

- India’s BoP position improved from US$ 412.9 bn of forex reserves in end-March, 2019 to US$ 433.7 bn in end-September 2019.

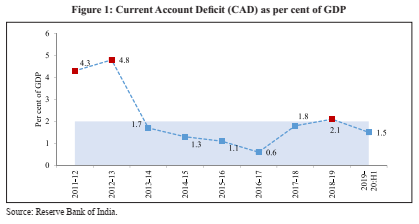

- Current account deficit (CAD) narrowed from 2.1% in 2018-19 to 1.5% of GDP in H1 of 2019-20.

- Top export items: Petroleum products, precious stones, drug formulations & biologicals, gold, and other precious metals.

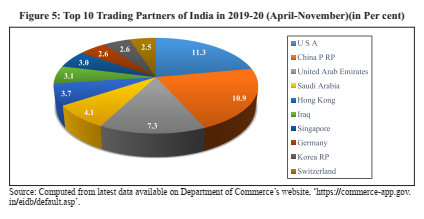

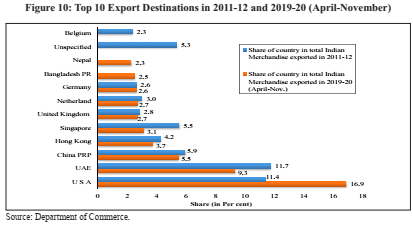

- Largest export destinations in 2019-20 (April-November): United States of America (USA), followed by the United Arab Emirates (UAE), China and Hong Kong.

- Top import items: Crude petroleum, gold, petroleum products, coal, coke & briquittes.

- India’s imports continue to be the largest from China, followed by the USA, UAE and Saudi Arabia.

- According to the World Bank’s Logistics Performance Index, India ranks 44thin 2018 globally, up from 54thrank in 2014.

- Net FDI inflows continued to be buoyant in 2019-20 attracting US$ 24.4 bn in the first eight months, higher than the corresponding period of 2018-19.

- Net FPI in the first eight months of 2019-20 stood at US$ 12.6 bn.

- Net remittances from Indians employed overseas continued to increase, receiving US$ 38.4 billion in H1 of 2019-20 which is more than 50% of the previous year level.

INTRODUCTION:

- India’s external sector gained further stability in the first half of 2019-20, witnessing improvement in the Balance of Payments (BoP) position. India’s foreign reserves are comfortably placed at US$ 461.2 billion as of 10th January 2020.

- The improvement in BoP was anchored by the narrowing of current account deficit (CAD) from 2.1% in 2018- 19 to 1.5% of GDP in H1 of 2019-20.

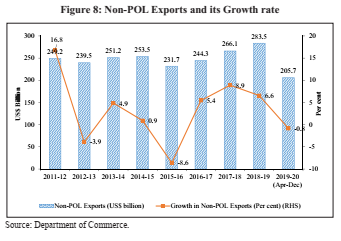

- Export growth remains subdued with external demand weakened by the slowdown in global investment, output, and heightened trade tensions, notwithstanding resilient service exports.

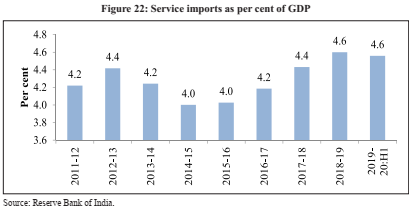

- An increase in service imports is inevitable with increasing foreign direct investment (FDI) and ‘Make in India’.

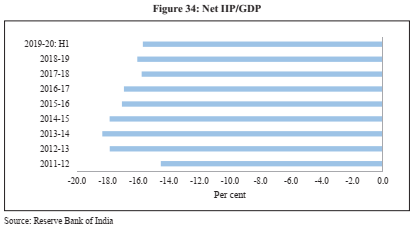

- India’s Net International Investment Position (NIIP) to GDP ratio has also improved compared to 2018-19.

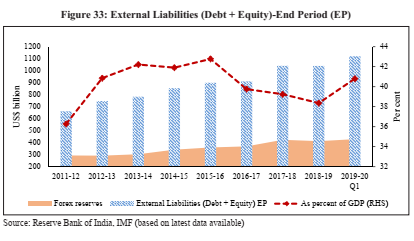

After witnessing a significant decline since 2014-15, India’s external liabilities (debt and equity) to GDP have increased at the end of June 2019 primarily driven by an increase in FDI, portfolio flows and external commercial borrowings (ECBs).

GLOBAL ECONOMIC ENVIRONMENT:

Increasing Trade Protectionism and Slowing down of Global Output:

- 2019-20 has closed with growth in world output on a downward trajectory. The World Economic Outlook (WEO) has projected growth in world output at 2.7% in 2020, down from 3.3 in 2019.

- Heightened US-China trade tensions have been stated as one of the reasons behind the global slowdown that has spilled into other economies including India through the channel of exports.

- The WEO also clarifies that trade-protectionism will only divert bilateral trade imbalances from one country to another as the root cause of trade deficits is the macroeconomic imbalance.

- US-Iran relations have also affected the trajectory of global economic growth.

- The WEO accordingly advises that at the multi-lateral level, the main priority is for countries to resolve trade disagreements cooperatively, without raising distortionary barriers that would further destabilize a slowing global economy.

- These developments increase the vulnerability of the external sector of emerging market economies like India, which are dependent on crude imports for fuelling their economic growth.

India’s Balance of Payments (BoP):

- India’s BoP position improved from US$ 412.9 bn of forex reserves in end-March, 2019 to US$ 433.7 bn in end September 2019.

- Current Account Deficit (CAD) narrowed from 2.1% in 2018-19 to 1.5% of GDP in H1 of 2019-20. Foreign reserves stood at US$ 461.2 bn as of10thJanuary 2020.

GLOBAL TRADE:

- In sync with an estimated 2.9% growth in global output in 2019, global trade is estimated to grow at 1.0% after having peaked in 2017 at 5.7%.

- However, it is projected to recover to 2.9% in 2020 with a recovery in global economic activity.

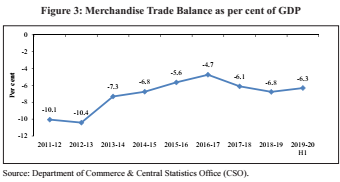

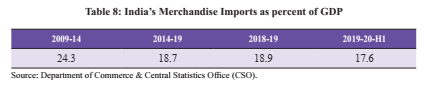

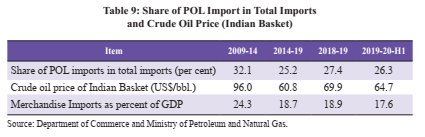

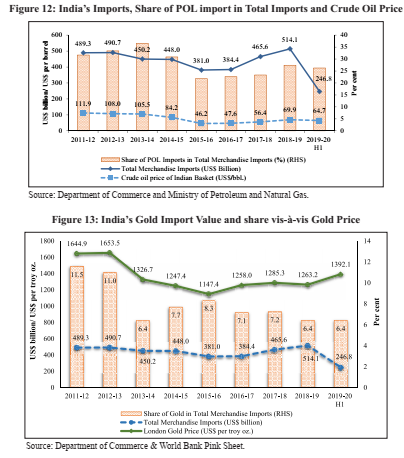

- India’s merchandise trade balance improved from 2009-14 to 2014-19, although most of the improvement in the latter period was due to more than 50% decline in crude prices in 2016-17.

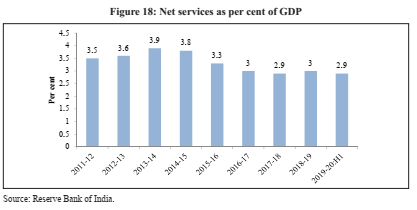

- India’s top five trading partners continue to be the USA, China, UAE, Saudi Arabia, and Hong Kong.

EXPORTS:

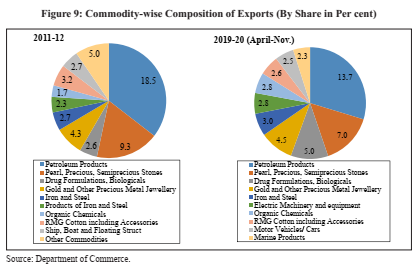

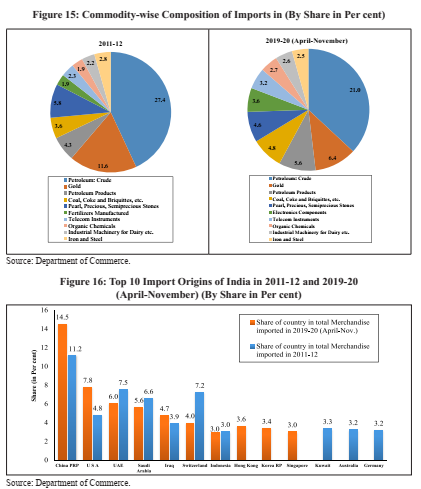

- Top export items: Petroleum products, precious stones, drug formulations & biologicals, gold, and other precious metals.

- Largest export destinations in 2019-20 (April-November): United States of America (USA), followed by the United Arab Emirates (UAE), China and Hong Kong.

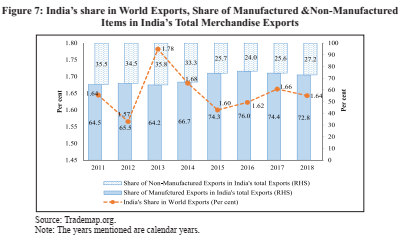

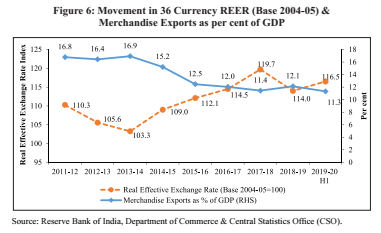

- The merchandise exports to GDP ratio declined, entailing a negative impact on the BoP position.

- The slowdown of world output had an impact on reducing the export to GDP ratio, particularly from 2018-19 to H1 of 2019-20.

IMPORTS:

- Top import items: Crude petroleum, gold, petroleum products, coal, coke &briquettes.

- India’s imports continue to be the largest from China, followed by the USA, UAE and Saudi Arabia.

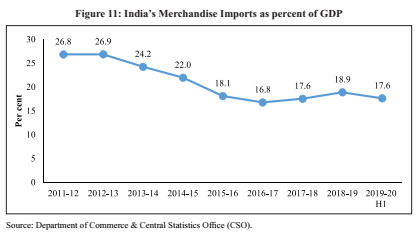

- Merchandise imports to GDP ratio declined for India, entailing a net positive impact on BoP.

- Large Crude oil imports in the import basket correlate India’s total imports with crude prices. As crude price raises so does the share of crude in total imports, increasing imports to GDP ratio.

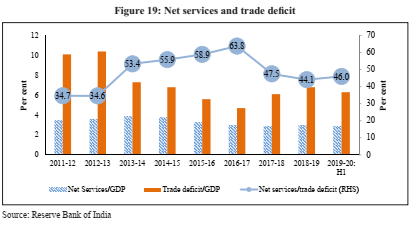

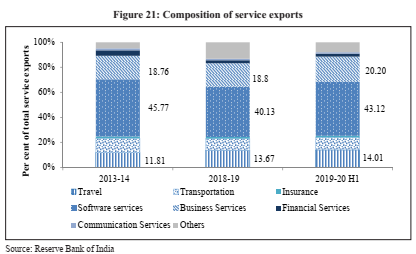

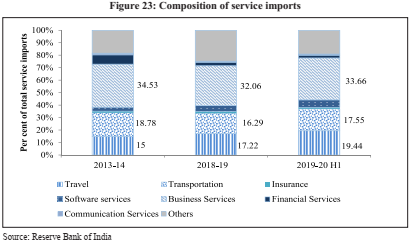

NET SERVICES:

- Net services as a proportion of GDP reflects the net impact of service exports and imports on BoP. India’s net services surplus has been steadily declining in relation to GDP.

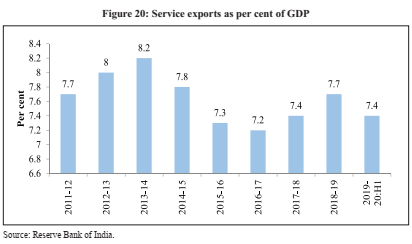

- Service Exports: An increase in service exports to GDP ratio has a net positive impact on the BoP position. India’s service exports have however consistently hovered between 7.4% to 7.7% of the GDP, reflecting the steadiness of this source in contributing to the stability of BoP.

LOGISTICS INDUSTRY OF INDIA:

- Currently estimated to be around US$ 160 billion.

- Expected to touch US$ 215 billion by 2020.

- According to the World Bank’s Logistics Performance Index, India ranks 44thin 2018 globally, up from 54thrank in 2014.

FDI & FPI

- Net FDI inflows continued to be buoyant in 2019-20 attracting US$ 24.4 bn in the first eight months, higher than the corresponding period of 2018-19.

- Net FPI in the first eight months of 2019-20 stood at US$ 12.6 bn.

- Net remittances from Indians employed overseas continued to increase, receiving US$ 38.4 billion in H1 of 2019-20 which is more than 50% of the previous year level.

- An increase in net remittances improves the BoP position. Net remittances from Indians employed overseas has been constantly increasing year after year and have continued doing so with the amount received in the first half of 2019-20 being more than 50% of the total receivables in 2018-19.

EXTERNAL DEBT:

- Remains low at 20.1% of GDP at the end of September 2019.

- After a significant decline since 2014-15, India’s external liabilities (debt and equity) to GDP increased at the end of June 2019 primarily by an increase in FDI, portfolio flows and external commercial borrowings (ECBs).

NET INTERNATIONAL INVESTMENT POSITION (NIIP):

- NIIP measures the gap between a nation’s stock of foreign assets and foreigner’s stock of that nation’s assets at a specific point in time.

- Changes in the NIIP/GDP ratio nets out the impact of an investment made by the country abroad from the external liabilities borne by the country, thereby measuring the net changes in the debt and equity servicing burden in relation to GDP.

- The surge in net FDI inflows has worsened the absolute NIIP level from 2009-14 to 2014-19.

CONCLUSION:

- Government policies are expected to further lift restrictions on FDI inflows, which will continue to increase the stability of sources funding the current account deficit.

- From a macroeconomic perspective, the deterioration of CAD may be contained if consumption slows down in the economy, while an increase in investment and exports become the new drivers of the Indian economy.