Focus: GS-III Indian Economy

Why in news?

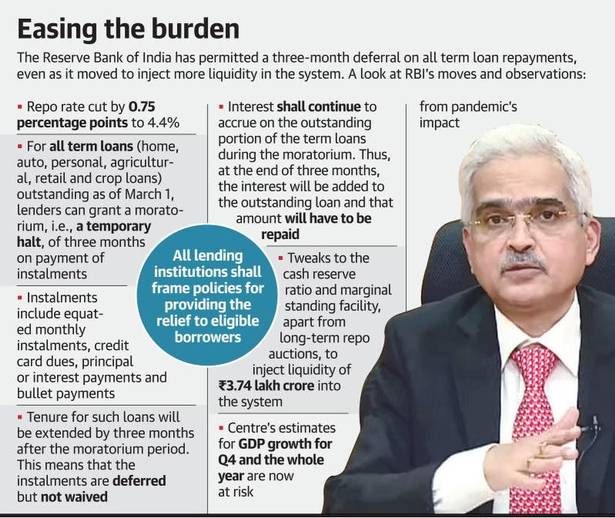

- The Reserve Bank of India (RBI) has opened up the liquidity floodgates for banks even as it reduced the key interest rate sharply by 75 bps and allowed equated monthly instalments (EMIs) to be deferred by three months in a move to fight the economic impact of the countrywide lockdown to check the spread of novel coronavirus.

- The meeting of the Monetary Policy Committee (MPC) which was scheduled for March 31 and April 1,3, was advanced to March 27 due to the unprecedented crisis.

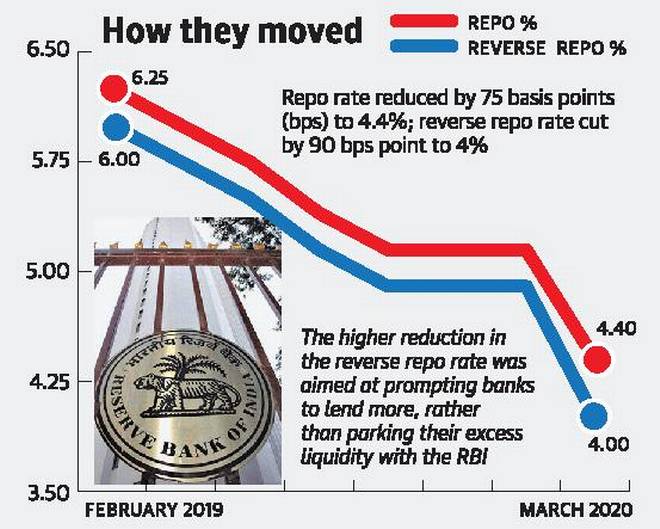

- The repo rate was reduced to by 75 bps 4.4% while the reverse repo rate was cut by 90 bps point to 4%.

- The higher reduction in the reverse repo rate was aimed at prompting banks to lend more rather than keeping their excess liquidity with the RBI.

What RBI had to say?

- Everything hinges on the depth of the COVID-19 outbreak, its spread and its duration.

- Clearly, a war effort has to be mounted to combat the virus, involving both conventional and unconventional measures.

Highlights of what RBI has done:

- While cutting benchmark rates, the RBI has continued with its accommodative stance.

- Apart from cutting the repo rate, RBI has also reduced the cash reserve ratio of banks which released ₹1.37 lakh crore liquidity.

- This, along with other measures, will see an infusion of ₹3.74 lakh crore into the banking system.

- RBI has also allowed banks to defer payment of EMIs on home, car, personal loans as well as credit card dues for three months till May 31.

- Since non-payment will not lead to non-performing asset classification by banks, there will be no impact on credit score of the borrowers.

Home and auto EMIs, credit card dues deferred by three months

- In a move to protect borrowers financially amid the nationwide lockdown, the Reserve Bank of India (RBI) has allowed all banks and financial institutions, including non-banking finance companies, to extend a three-month moratorium period on the instalments due between March 1, 2020 and May 31, 2020 for all term loans.

- The relaxation is also applicable on consumer loans such as auto loans, home loans and personal loans, as well as credit card outstanding dues.

- A consumer may now choose not to pay the monthly equated instalments on their loans for the next three months.

- The repayment schedule for such loans, as also the residual tenor, will be shifted across the board by three months after the moratorium period.

- The three-month moratorium on all term loan instalments, along with deferment of interest on working capital, will help mitigate debt servicing burden due to COVID-19 disruption, and prevent transmission of financial stress to various sectors of the economy.

Liquidity floodgates opened

- In a move to infuse sufficient liquidity into the banking system, the Reserve Bank of India has reduced the cash reserve ratio (CRR) requirement by 100 bps, increased the cap for liquidity available under the marginal standing facility, and will auction long-term repo of ₹1 lakh crore.

- The monetary policy committee reduced the repo rate by 75 bps to 4.4% and consequently the Marginal Standing Facility (MSF) rate was reduced to 4.65%.

- These three measures will infuse ₹3.74 lakh crore into the banking system.

- The cash reserve ratio — the proportion of liabilities which a bank has to set aside as cash — has been reduced from 4% to 3%.

- The 100 bps reduction in CRR will free up ₹1.37 lakh crore liquidity for the banks.

- Banks do not earn any interest for maintaining CRR balance. With this reduction, they can deploy the liquidity in interest-earning assets.

- RBI also increased liquidity available to banks under the marginal standing facility from 2% of the statutory liquidity ratio (SLR) to 3% with immediate effect.

- This measure should provide comfort to the banking system by allowing it to avail itself of an additional ₹1,37,000 crore of liquidity under the LAF window in times of stress at the reduced MSF rate announced in the MPC’s resolution.

Monetary Policy Committee (MPC)

- The Monetary Policy Committee of India is responsible for fixing the benchmark interest rate in India.

- The meetings of the Monetary Policy Committee are held at least 4 times a year and it publishes its decisions after each such meeting.

- The committee comprises six members – three officials of the Reserve Bank of India and three external members nominated by the Government of India.

- They need to observe a “silent period” seven days before and after the rate decision for “utmost confidentiality”.

- The Governor of Reserve Bank of India is the chairperson ex officio of the committee.

- The Reserve Bank of India Act, 1934 was amended by Finance Act (India), 2016 to constitute MPC which will bring more transparency and accountability in fixing India’s Monetary Policy.

- The monetary policy are published after every meeting with each member explaining his opinions.

- The committee is answerable to the Government of India if the inflation exceeds the range prescribed for three consecutive months.

- Key decisions pertaining to benchmark interest rates used to be taken by the Governor of Reserve Bank of India alone prior to the establishment of the committee.

- The Governor of RBI is appointed and can be disqualified by the Government anytime.

Cash Reserve Ratio (CRR)

- The Reserve Bank of India or RBI mandates that banks store a proportion of their deposits in the form of cash so that the same can be given to the bank’s customers if the need arises.

- The percentage of cash required to be kept in reserves, vis-a-vis a bank’s total deposits, is called the Cash Reserve Ratio.

- The cash reserve is either stored in the bank’s vault or is sent to the RBI.

- Banks do not get any interest on the money that is with the RBI under the CRR requirements.

- The Cash Reserve Ratio in India is decided by RBI’s Monetary Policy Committee in the periodic Monetary and Credit Policy.

- CRR is one of the major weapons in the RBI’s arsenal that allows it to maintain a desired level of inflation, control the money supply, and also liquidity in the economy.

- The lower the CRR, the higher liquidity with the banks, which in turn goes into investment and lending and vice-versa.

- Higher CRR can also negatively impact the economy as lesser availability of loanable funds, in turn, slows down investment. It thereby reduces the supply of money in the economy.

Statutory Liquidity Ratio (SLR)

- Every bank must have a specified portion of their Net Demand and Time Liabilities (NDTL) in the form of cash, gold, or other liquid assets by the day’s end. The ratio of these liquid assets to the demand and time liabilities is called the Statutory Liquidity Ratio (SLR).

- An increase in the ratio constricts the ability of the bank to inject money into the economy.

- RBI is also responsible for regulating the flow of money and stability of prices to run the Indian economy.

- Statutory Liquidity Ratio is one of its many monetary policies for the same.

- SLR (among other tools) is instrumental in ensuring the solvency of the banks and cash flow in the economy.

Difference between SLR & CRR

Both SLR and CRR are the components of the monetary policy.

The following table gives a glimpse into the dissimilarities:

| Statutory Liquidity Ratio (SLR) | Cash Reserve Ratio (CRR) |

| In the case of SLR, banks are asked to have reserves of liquid assets which include both cash and gold. | The CRR requires banks to have only cash reserves with the RBI |

| Banks earn returns on money parked as SLR | Banks don’t earn returns on money parked as CRR |

| SLR is used to control the bank’s leverage for credit expansion. | The Central Bank controls the liquidity in the Banking system with CRR. |

| In the case of SLR, the securities are kept with the banks themselves which they need to maintain in the form of liquid assets. | In CRR, the cash reserve is maintained by the banks with the Reserve Bank of India. |

Source: https://cleartax.in/s/slr

Marginal Standing Facility (MSF)

- Marginal Standing Facility (MSF) is a window for banks to borrow from the Reserve Bank of India in an emergency situation when inter-bank liquidity dries up completely.

- Banks borrow from the central bank by pledging government securities at a rate higher than the repo rate under liquidity adjustment facility or LAF in short.

- The MSF rate is pegged 100 basis points or a percentage point above the repo rate. Under MSF, banks can borrow funds up to one percentage of their net demand and time liabilities (NDTL).

Liquidity Adjustment Facility (LAF)

- Liquidity Adjustment Facility (LAF) is a monetary policy tool which allows banks to borrow money through repurchase agreements.

- LAF is used to aid banks in adjusting the day to day mismatches in liquidity.

- LAF consists of repo and reverse repo operations.

- Repo or repurchase option is a collaterised lending i.e., banks borrow money from Reserve bank of India to meet short term needs by selling securities to RBI with an agreement to repurchase the same at predetermined rate and date.

Differences between LAF and MSF

| LAF- Liquidity Adjustment Facility | MSF- Marginal Standing Facility |

| This is for short term Minimum bidding amount is 5 cr. All clients of RBI are eligible to bid. Bank cannot sell Government security to RBI that is part of bank’s SLR quota. Bank can borrow any amount of money as long as it has the securities to sell. | This is for long term Minimum bidding amount is 1 cr. Only scheduled commercial banks can bid. Bank can sell the Government security from its SLR quota to RBI. Bank can maximum borrow upto 2% of its NDTL. |