Context:

The GST Council met in Lucknow on 17th September 2021, the first physical meeting in nearly two years, to take key decisions.

Relevance:

GS-II: Social Justice (Government Interventions and Policies, Issues arising out of the design and implementation of Government Policies)

Dimensions of the Article:

- What are the key decisions made by GST Council?

- 10: Latest Decision On Compensation cess mechanism

- Background: What is GST Compensation Cess?

- 11: Latest Decision On e-commerce operators

Click Here to read about GST, GST Council and its functions – and also the consideration of bringing fuel prices under GST

What are the key decisions made by GST Council?

- On Covid-19 Treatment: Existing concessional rates for Covid-19 medicines: Remdesivir (5 per cent), Tocilizumab (nil), Amphotericin B (nil), and anti-coagulants like Heparin (5 per cent) have been extended till December 2021. Along with this, a reduction of GST rate to 5 per cent on more Covid-19 treatment drugs like Itolizumab, Favipiravir etc., was also extended. However, the concessional tax for medical equipment will end on September 2021 as decided previously.

- On other medicines: The Council also decided to remove GST on the import of muscular atrophy drugs like Zolgensma and Viltepso, which cost crores of rupees. The GST rate for Keytruda, used for the treatment of cancer, has been cut to 5 per cent from 12 per cent.

- On Fortified rice: The Council also cut GST rates on fortified rice kernels to 5 per cent from 18 per cent.

- On Biodiesel: The Council also cut GST rates on bio-diesel for blending in diesel to 5 per cent from 12 per cent.

- On Ores and related: GST on ores and concentrates of metals such as iron, copper, aluminum, and zinc has been increased from 5 per cent to 18 per cent, and that on specified renewable energy devices and parts from 5 per cent to 12 per cent.

- On Packaging and other waste generating products: Cartons, boxes, bags, and packing containers of paper will now attract a uniform 18 per cent tax in place of the 12 per cent and 18 per cent rates. Waste and scrap of polyurethanes and other plastics will also see tax going up to 18 per cent from 5 per cent currently.

- On Soft-drinks: The rate for carbonated fruit beverages and carbonated beverages with fruit juice will attract a GST rate of 28 per cent, plus compensation cess of 12 per cent.

- On inclusion of fuel under GST: The Council discussed the issue only because the Kerala High Court had asked it, but felt it was not the right time to include petroleum products under GST.

- On inverted duty structure: The Council will also look at rate rationalisation under the inverted duty structure, and compliance measures through e-way bill and composition schemes. The Council has decided to set up a GoM to examine the issue of correction of inverted duty structure for major sectors; rationalise the rates and review exemptions from the point of view of revenue augmentation.

10: Latest Decision On Compensation cess mechanism

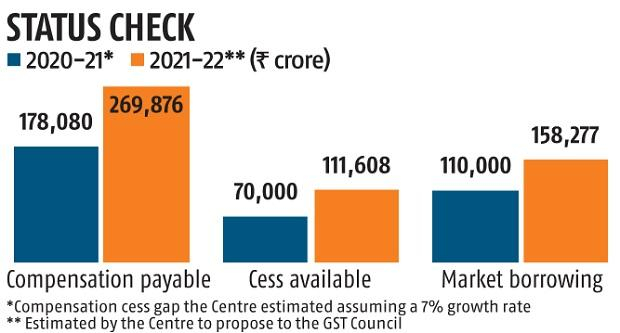

- The Council also decided to put an end date of June 2022 to the compensation mechanism, as mandated in law.

- The levy of compensation cess will continue from July 2022 onwards till March 2026 to service the borrowing, which had been resorted to in order to bridge the compensation gap in the years 2020-21 and 2021-22.

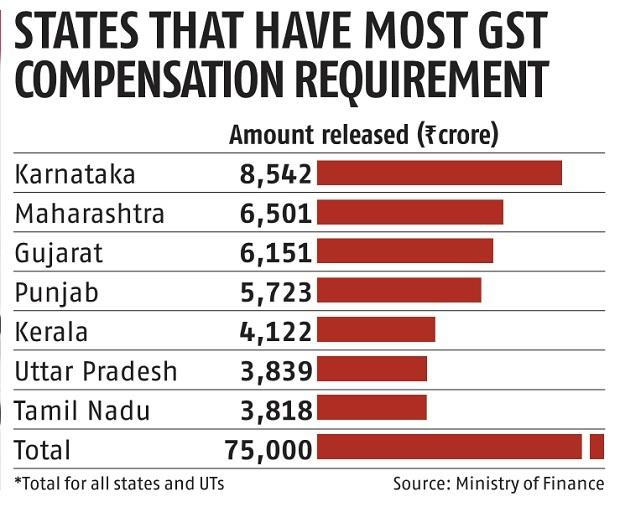

- The debt for making compensation payments to states is estimated to be around Rs 2.7 lakh crore.

- In the previous GST Council meeting, it had been decided that beyond July 2022, the collection of cess would be for “payment of loans taken”. Beyond July 2022, the cess that the government collecting, as agreed in the 43rd Council meeting, is for the purpose of repaying the loans given to states since 2020.

Background: What is GST Compensation Cess?

GST was implemented through the GST (101st Amendment Act), 2016 as a long pending indirect tax reform. It is a single tax that replaces multiple other indirect taxes. The Centre lost out on its power to levy taxes such as excise duty, while the States could no longer levy entry tax, VAT etc. To allay the fears of States regarding loss of revenue, following mechanism was made:

GST (Compensation to States) Act, 2017 was enacted under which:

- The percentage of annual revenue growth of a State has been projected to be 14%. If the annual revenue growth of a State is less than 14%, the State is entitled to receive compensation under the statute.

- The compensation payable to a State shall be provisionally calculated and released at the end of every two months period.

- The generation of revenue under the Act would happen through a GST Compensation Cess:

- The cess comprises the cess levied on sin and luxury goods for five years.

- The entire cess collected during the year is required to be credited to a non-lapsable Fund (the GST Compensation Cess Fund).

- The collected compensation cess flows into the CFI and is then transferred to the Public Account of India, where the GST compensation cess fund has been created.

Issue with GST Compensation Cess

The issue arose when payments due for August-September 2019 were delayed. Since then, all subsequent payouts have seen cascading delays. The problem has aggravated and further compounded due to following reasons:

- Persistent Economic Slowdown: The slowdown has impacted the demand and consumption levels and has thus dented the overall GST collections (both Centre and States).

- Effect of the Pandemic: The pandemic has given an economic shock to the Indian Economy which has dented the tax collection expectations (including the collections from GST Compensation Cess) of both Centre and States.

- Estimation of 14% revenue growth unrealistic: The high rate of 14%, which has compounded since 2015- 16, has been seen as delinked from economic realities. In the initial meetings of the GST Council, a revenue growth rate of 10.6% (the average all-India growth rate in the three years preceding 2015-16) was proposed but 14% revenue growth was accepted “in the spirit of compromise”.

As a result of these issues, the stalemate reached at a point where States were looking at the GST shortfall of Rs. 30,000 crore and the Centre being in no position to provide for it.

11: Latest Decision On e-commerce operators

- Effective January 1 2022, the Council has decided to make e-commerce operators engaged in restaurant services liable for payment of tax. This will essentially shift the responsibility of paying the 5 per cent GST to the aggregators from the restaurants.

- As a result of this, the restaurants will also have to mandatorily register themselves as is done by e-commerce sellers.

Why was this decision taken?

- Currently, if a customer orders food, for example, from Restaurant A using Swiggy or Zomato, the food delivery platform collects the 5 per cent tax on food from the customer and passes it on to the restaurant.

- However, the government believes that several restaurants have not deposited their tax despite them recording high turnover.

Does anything change for the consumer?

- No, since there is no new tax that has been introduced, the consumer will continue to pay the 5 per cent rate on the food they order online.

- The proposal of the GST Council, which got approved Friday, also pegged to bring the delivery services under the tax net, but it determined that since the customer does not directly avail the services of a delivery executive, nor do they have the choice of which delivery executive services them, the responsibility for paying the tax on delivery services will lie with the food-delivery apps.

-Source: The Hindu