Focus: GS-III Indian Economy

Drop in net tax collection

The net direct tax collection for the FY 2019-20 was less than the net direct tax collection for the FY 2018-19.

This fall in the collection of direct taxes is on expected lines and is temporary in nature due to the historic tax reforms undertaken and much higher refunds issued during the FY 2019-20.

Tax reforms undertaken

I- Reduction in corporate tax rate for all existing domestic companies

Taxation Laws (Amendment) Ordinance 2019 which provided a concessional tax regime of 22% for all existing domestic companies from FY 2019-20 if they do not avail any specified exemption or incentive.

Further, such companies have also been exempted from payment of Minimum Alternate Tax (MAT).

II- Incentive for new manufacturing domestic companies

Taxation Laws (Amendment) Ordinance 2019 has drastically reduced the tax rate to 15% for new manufacturing domestic company if such company does not avail any specified exemption or incentive.

These companies have also been exempted from payment of Minimum Alternate Tax (MAT).

III- Reduction in MAT rate

Minimum Alternate Tax (MAT) has also been reduced from 18.5% to 15%.

IV- Exemption from income-tax to individuals earning income up to Rs. 5 lakh and increase in standard deduction

Finance Act, 2019 exempted an individual taxpayer with taxable income up to Rs. 5 lakh by providing 100% tax rebate and enhanced the standard deduction from Rs. 40,000 to Rs. 50,000.

V- Abolition of Dividend Distribution Tax (DDT)

The Finance Act, 2020 removed the Dividend Distribution Tax under which the companies are not required to pay DDT – to increase the attractiveness of the Indian Equity Market and to provide relief to a large class of investors in whose case dividend income is taxable at the rate lower than the rate of DDT.

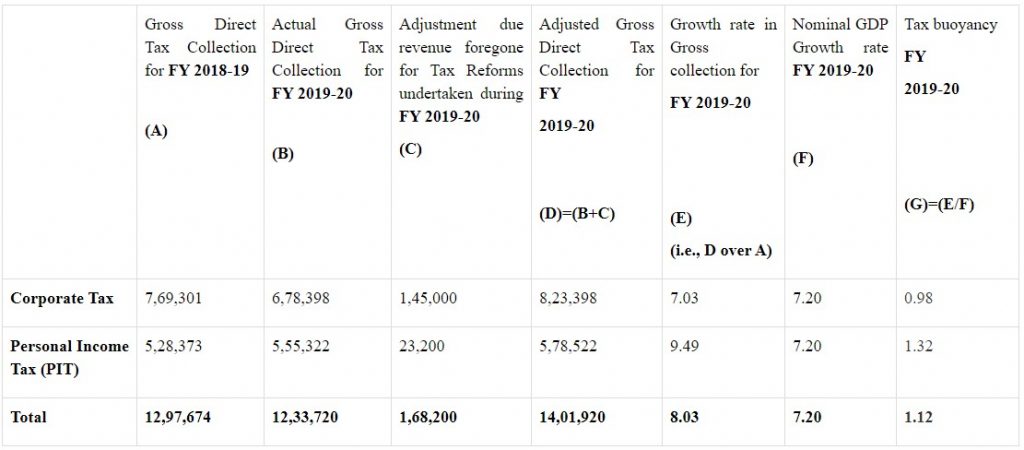

Tax Buoyancy for 2019-20

- These buoyancies indicate that the growth trajectories of both the arms of direct taxes, i.e., Corporate Tax and PIT are intact and are rising steadily.

- The higher growth rate in direct taxes as compared to growth rate in the GDP even in these challenging times proves that recent efforts for the widening of the tax base undertaken by the Government are yielding results.

Other Steps taken to improve Indian Economic activities

VI- Vivad se Vishwas

Direct Tax Vivad se Vishwas Act, 2020 was enacted under which the declarations for settling disputes are currently being filed.

The act provides for resolution of pending tax disputes which benefits the Government by generating timely revenue and also benefits the taxpayers as it will bring down mounting litigation costs and efforts can be better utilized for expanding business activities.

VII- Faceless E-assessment and appeals Scheme

Faceless E-assessment provides for a new scheme for making assessment by eliminating the interface between the Assessing Officer and the assessee, optimizing use of resources through functional specialization and introducing the team-based assessment.

VIII- Document Identification Number (DIN)

In order to bring efficiency and transparency in the functioning of the Income Tax Department, Every communication of the Department mandatorily have a computer-generated unique document identification number (DIN).

IX- Encouraging digital transactions

Various measures have been taken which include reduction in rate of presumptive profit on digital turnover, removal of MDR charges on prescribed modes of transactions, reducing the threshold for cash transactions, prohibition of certain cash transactions, etc.

X- Expansion of scope of TDS/TCS

For widening the tax base, several new transactions were brought into the ambit of Tax Deduction at Source (TDS) and Tax Collection at Source (TCS). These transactions include huge cash withdrawal, foreign remittance, purchase of luxury car, e-commerce participants, sale of goods, acquisition of immovable property, etc.

XI- Simplification of compliance norms for Start-ups

Start-ups have been provided hassle-free tax environment which includes simplification of assessment procedure, exemptions from Angel-tax, constitution of dedicated start-up cell etc.