Context:

Former RBI governor Raghuram Rajan and ex-deputy governor Viral Acharya argued against allowing companies to own banks because it would allow non-financial businesses to gain easy access to financing and encourage connected lending and because it could lead to further concentration of economic and political power in certain business houses.

Relevance:

GS Paper 2: Indian Economy (issues re: planning, mobilisation of resources, growth, development, employment); Inclusive growth and issues therein.

Mains Questions

- The banking sector needs reform but the recommendation of corporate-owned banks is neither ‘big bang’ nor risk-free. Critically comment. 15 marks

- Banking sector needs more competition. But allowing corporates in without strong regulation could heighten systemic risk. Discuss. 15 marks

Dimensions of the article

- Status of the Banking sector in India

- Key points of the Internal Working Group of the Reserve Bank of India

- Issues related to the corporate houses be given bank licences

- Way Forward

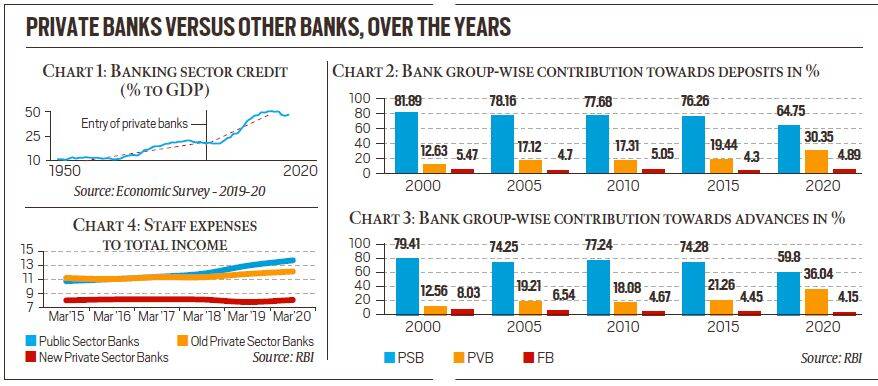

Status of the Banking Sector in India

- The banking system in any country is of critical importance for sustaining economic growth. India’s banking system has changed a lot since Independence when banks were owned by the private sector, resulting in a “large concentration of resources in the hands of a few business families”.

- To achieve “a wider spread of bank credit, prevent its misuse, direct a larger volume of credit flow to priority sectors and to make it an effective instrument of economic development”, the government resorted to the nationalisation of banks in 1969 (14 banks) and again in 1980 (6 banks).

- With economic liberalisation in the early 1990s, the economy’s credit needs grew and private banks re-entered the picture. This had a salutary impact on credit growth.

- However, even after three decades of rapid growth, “the total balance sheet of banks in India still constitutes less than 70 per cent of the GDP, which is much less compared to global peers” such as China, where this ratio is closer to 175%.

- Moreover, domestic bank credit to the private sector is just 50% of GDP when in economies such as China, Japan, the US and Korea it is upwards of 150 per cent. In other words, India’s banking system has been struggling to meet the credit demands of a growing economy. There is only one Indian bank in the top 100 banks globally by size. Further, Indian banks are also one of the least cost-efficient.

Clearly, India needs to bolster its banking system if it wants to grow at a fast clip. In this regard, it is crucial to note that public sector banks have been steadily losing ground to private banks. Private banks are not only more efficient and profitable but also have more risk appetite.

Key points of the Internal Working Group of the Reserve Bank of India

Entry of Corporates into Banking Space:

- Large corporates and industrial houses may be allowed as promoters of banks only after necessary amendments to the Banking Regulation Act, 1949.

- A promoter is an individual or organization that helps raise money for some type of investment activity.

- This is to prevent connected lending and exposures between the banks and other financial and non-financial group entities.

- Connected lending is modelled as a situation in which the bank’s controlling owner extends loans of inferior quality at lower interest rates to himself or his connected parties.

- Credit exposure is a measurement of the maximum potential loss to a lender if the borrower defaults on payment.

- The RBI has been against allowing corporate houses to set up or run commercial banks due to their poor track record on governance and credit disbursement.

- Corporate houses routinely delay payments to banks and the system has no in-built incentives or disincentives for orderly debtor behaviour.

Conversion of NBFCs into Banks:

- Well-run large NBFCs, with an asset size of Rs. 50,000 crore and above, including those which are owned by a corporate house, may be considered for conversion into banks subject to completion of 10 years of operations and meeting due diligence criteria and compliance with additional conditions specified in this regard.

Hike in Promoters’ Stake:

- The cap on promoters’ stake in the long run (15 years) may be raised from the current level of 15% to 26% of the paid-up voting equity share capital of the bank.

- On non-promoter shareholding, the panel has suggested a uniform cap of 15% of the paid-up voting equity share capital of the bank for all types of shareholders.

Hike in Minimum Capital for New Banks:

- The minimum initial capital requirement for licensing new banks should be enhanced from Rs. 500 crore to Rs. 1,000 crore for universal banks and from Rs. 200 crore to Rs. 300 crore for small finance banks.

- Universal Banks combine the three main services of banking viz. wholesale banking, retail banking, and investment banking under one roof. For example, Deutsche Bank, Bank of America, HSBC, etc.

Payments Banks’ Conversion into Small Finance Bank:

- For payments banks intending to convert to a Small Finance Bank (SFB), a track record of 3 years of experience as payments bank may be considered as sufficient.

- Payments banks (Airtel Payments Bank, India Post Payments Bank, etc.) are like any other banks, but operating on a smaller or restricted scale.

- Small Finance Banks are the financial institutions which provide financial services to the unserved and unbanked region of the country.

Harmonisation and Uniformity in Different Licensing Guidelines:

- The RBI should take steps to ensure harmonisation and uniformity in different licensing guidelines, to the extent possible.

- Whenever new licensing guidelines are issued, if new rules are more relaxed, the benefit should be given to existing banks, and if new rules are tougher, legacy banks should also conform to new tighter regulations, but a non-disruptive transition path may be provided to affected banks.

Non Operative Financial Holding Company:

- NOFHC should continue to be the preferred structure for all new licenses to be issued for universal banks. However, it should be mandatory only in cases where the individual promoters, promoting entities and converting entities have other group entities.

- NOFHC is a financial institution through which promoter/promoter groups will be permitted to set up a new bank.

- Entities or groups in the private sector, public sector and NBFCs can set up these wholly-owned NOFHCs.

Issues related to the corporate houses be given bank licences

As the report notes, the main concerns are interconnected lending, concentration of economic power and exposure of the safety net provided to banks (through guarantee of deposits) to commercial sectors of the economy.

Increasing concentration of economic power:

- Corporate houses can easily turn banks into a source of funds for their own businesses.

- In addition, they can ensure that funds are directed to their cronies.

- They can use banks to provide finance to customers and suppliers of their businesses.

- Adding a bank to a corporate house thus means an increase in concentration of economic power.

- Just as politicians have used banks to further their political interests, so also will corporate houses be tempted to use banks set up by them to enhance their clout.

Exposure of the safety net provided to banks:

- The banks owned by corporate houses will be exposed to the risks of the non-bank entities of the group. If the non-bank entities get into trouble, sentiment about the bank owned by the corporate house is bound to be impacted. Depositors may have to be rescued through the use of the public safety net.

Interconnected Lending:

- The Internal Working Group believes that before corporate houses are allowed to enter banking, the RBI must be equipped with a legal framework to deal with interconnected lending and a mechanism to effectively supervise conglomerates that venture into banking.

- It is naive to suppose that any legal framework and supervisory mechanism will be adequate to deal with the risks of interconnected lending in the Indian context.

- Corporate houses are adept at routing funds through a maze of entities in India and abroad. Tracing interconnected lending will be a challenge.

- Monitoring of transactions of corporate houses will require the cooperation of various law enforcement agencies. Corporate houses can use their political clout to thwart such cooperation.

- The RBI can only react to interconnected lending ex-post, that is, after substantial exposure to the entities of the corporate house has happened. It is unlikely to be able to prevent such exposure.

- Suppose the RBI does latch on to interconnected lending. How is the RBI to react? Any action that the RBI may take in response could cause a flight of deposits from the bank concerned and precipitate its failure. The challenges posed by interconnected lending are truly formidable.

Regulator credibility at stake

- Pitting the regulator against powerful corporate houses could end up damaging the regulator. The regulator would be under enormous pressure to compromise on regulation. Its credibility would be dented in the process. This would indeed be a tragedy given the stature the RBI enjoys today.

Moreover, The Committee on Financial Sector Reforms (2008) had set its face against the entry of corporate houses into banking. It had observed, “The Committee also believes it is premature to allow industrial houses to own banks. This prohibition on the ‘banking and commerce’ combine still exists in the United States today, and is certainly necessary in India till private governance and regulatory capacity improve.

Way Forward

India’s banking sector needs reform but corporate houses owning banks hardly qualifies as one. If the record of over-leveraging in the corporate world in recent years is anything to go by, the entry of corporate houses into banking is the road to perdition.

There is a strong case for liberalising entry into the banking sector, and to encourage the creation of big private banks capable of meeting the financing needs of the economy, a system of stringent checks and balances will need to be put in place before the central bank contemplates any such step.