Contents

- Govt. must constitute GST tribunal: SC

- Pact with rebel groups for peace in Karbi Anglong

- Crypto banking and decentralized finance

- Sukhet Model: LPG cylinders in exchange for cow dung

Govt. must constitute GST tribunal: SC

Context:

The Supreme Court said that the government had no option but to constitute the Goods and Services Tax (GST) Appellate Tribunal. The tribunal has not been constituted even four years after the central GST law was passed in 2016.

Relevance:

GS-III: Indian Economy (Taxation), GS-II: Governance (Government Policies and Initiatives), Prelims

Dimensions of the Article:

- What is GST and the GST Act?

- GST Council

- What is GST Appellate Tribunal?

- Constitution of the GST Appellate Tribunal

- Decisions taken by the Appellate Tribunal

- Can the Appellate Tribunal amend its own order?

What is GST and the GST Act?

GST is a destination-based indirect tax and is levied at the final consumption point. Under it, the final consumer of the goods and services bear the tax charged in the supply chain. GST is a transparent and fair system that prevents black money and corruption and promotes new governance culture.

GST Act

- Goods and Services Tax (GST) Act came into effect in 2017.

- Goods and Services Tax (GST) was introduced by the Government of India to boost the economic growth of India. GST is considered to be the biggest taxation reform in the history of the Indian economy.

- The power to make any changes in the GST law is in the hands of the GST Council. GST Council is headed by the Finance Minister. One hundred and first amendment act, 2016 introduced the GST in India in July 2017.

GST Council

- Goods & Services Tax Council is a constitutional body for making recommendations to the Union and State Government on issues related to Goods and Service Tax.

- As per Article 279A (1) of the amended Constitution, the GST Council has to be constituted by the President within 60 days of the commencement of Article 279A.

- The Constitution (One Hundred and Twenty-Second Amendment) Bill, 2016, for the introduction of Goods and Services Tax in the country was introduced in the Parliament and passed by Rajya Sabha on 3rd August 2016 and by Lok Sabha on 8th August 2016.

- GST Council is an apex member committee to modify, reconcile or procure any law or regulation based on the context of goods and services tax in India.

- The GST council is responsible for any revision or enactment of rule or any rate changes of the goods and services in India.

- The council contains the following members:

- Union Finance Minister (as chairperson)

- Union Minister of States in charge of revenue or finance (as members)

- The ministers of states in charge of finance or taxation or other ministers as nominated by each state’s government (as members).

Matters on which GST Council makes recommendations:

- Taxes, cesses, and surcharges levied by the Centre, States and local bodies which may be subsumed in the GST;

- Goods and services which may be subjected to or exempted from GST;

- Model GST laws, principles of levy, apportionment of IGST and principles that govern the place of supply;

- Threshold limit of turnover below which goods and services may be exempted from GST;

- Rates including floor rates with bands of GST;

- Special rates to raise additional resources during any natural calamity;

- Special provision with respect to Arunachal Pradesh, Jammu and Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand; and

- Any other matter relating to the goods and services tax, as the Council may decide.

What is GST Appellate Tribunal?

- The GST Appellate Tribunal (GSTAT) is the second appeal forum under GST for any dissatisfactory order passed by the First Appellate Authorities.

- The National Appellate Tribunal is also the first common forum to resolve disputes between the centre and the states.

- Being a common forum, it is the duty of the GSTAT to ensure uniformity in the redressal of disputes arising under GST.

- It holds the same powers as the court and is deemed Civil Court for trying a case.

- The Appellate Tribunal shall have the same powers as a court under the Code of Civil Procedure, 1908, for trying a case. It will be a deemed Civil Court.

Constitution of the GST Appellate Tribunal

- National Bench: The National Appellate Tribunal is situated in New Delhi, constitutes a National President (Head) along with 2 Technical Members (1 from Centre and State each)

- Regional Benches: On the recommendations of the GST Council, the government can constitute (by notification) Regional Benches, as required. As of now, there are 3 Regional Benches (situated in Mumbai, Kolkata and Hyderabad) in India.

- State Bench and Area Bench

Decisions taken by the Appellate Tribunal

- The Appellate Tribunal can confirm, modify or annul the decision or refer the case back to the First Appellate Authority [or the revisional authority].

- It may also refer the case back to the original adjudicating authority, with directions for a fresh decision after considering any additional evidence. The Appellate Tribunal shall give the decision within a period of one year from the appeal filing date. A copy of the order passed will be given to-

- The First Appellate Authority or the revisional authority, i.e.., the original adjudicating authority

- The appellant

- The jurisdictional Commissioner of CGST and

- The jurisdictional Commissioner of SGST.

How will decisions be taken by the Appellate Tribunal?

- The powers and functions of the Appellate Tribunal will be discharged by Benches. The State Bench & Area Bench shall consist of-

- 1 Judicial Member (Judicial)

- 1 CGST Member (Technical)

- 1 SGST Member (Technical)

- State President

- A single member can dispose of any case where the amount involved is below 5 lakhs.

Can the Appellate Tribunal amend its own order?

- The Appellate Tribunal can amend its order passed to rectify any apparent mistake within a period of three months from the date of the order.

- The mistake may be noticed by the Appellate Tribunal itself or may be brought to its notice by the Commissioner of GST or the other party to the appeal.

- Any amendment which will increase the tax liability or decrease the refund or input tax credit will be done only after a reasonable opportunity of being heard has been given.

- If the order is stayed by an order of a Court or Tribunal, the period of such stay shall be excluded from the one year period.

-Source: The Hindu

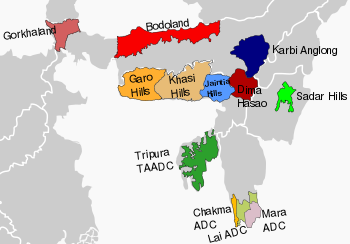

Pact with rebel groups for peace in Karbi Anglong

Context:

Moving to end decades of violence in Karbi Anglong in Assam, the Centre signed a tripartite agreement with five insurgent groups from the region and the state government.

Relevance:

GS-II: Polity and Constitution (Centre-State Relations, Inter-State Dispute Redressal Mechanisms)

Dimensions of the Article:

- About the Karbi Anglong Crisis

- Highlights of the Karbi-Anglong Peace Agreement

- Back to the Basics: About Autonomous District Councils (ADCs)

- Back to the Basics: Special Status of Sixth Schedule Areas

About the Karbi Anglong Crisis

- Located in central Assam, Karbi Anglong is the state’s largest district and a melting pot of ethnicities and tribal groups — Karbi, Dimasa, Bodo, Kuki, Hmar, Tiwa, Garo, Man (Tai speakers), Rengma Naga. Its diversity also generated different outfits and fuelled an insurgency that did not allow the region to develop.

- The Karbis are a major ethnic group of Assam, dotted by several factions and splinters. The history of the Karbi group has been marked by killings, ethnic violence, abductions and taxation since the late 1980s.

- Insurgent groups of Karbi Anglong district like People’s Democratic Council of Karbi Longri (PDCK), Karbi Longri NC Hills Liberation Front (KLNLF), etc. originated from the core demand of forming a separate state.

- Some of the other demands of the militant groups are:

- Inclusion of some areas into Karbi Anglong Autonomous Council (KAAC),

- Reservation of seats for Scheduled Tribes,

- More powers to the council,

- Inclusion of Karbi language in the Eighth Schedule,

- Financial package of Rs 1,500 crore.

Highlights of the Karbi-Anglong Peace Agreement

- 5 militant organizations (KLNLF, PDCK, UPLA, KPLT and KLF) laid down arms and more than 1000 of their armed cadres have given up violence and joined the mainstream of society.

- A special development package of Rs. 1000 crore will be allocated over five years by the Central Government and the Assam Government to take up special projects for the development of Karbi areas.

- This agreement will transfer as much autonomy as possible in exercising their rights to the Karbi Anglong Autonomous Council, without affecting the territorial and administrative integrity of Assam.

- A provision has been made in this agreement to rehabilitate the cadres of armed groups.

- The Government of Assam will set up a Karbi Welfare Council to focus on the development of the Karbi people living outside the KAAC area.

Back to the Basics: About Autonomous District Councils (ADCs)

- The Autonomous districts and regional councils (ADCs) are empowered with civil and judicial powers can constitute village courts within their jurisdiction to hear the trial of cases involving the tribes.

- Governors of states that fall under the Sixth Schedule specify the jurisdiction of high courts for each of these cases.

- Along with ADCs, the Sixth Schedule also provides for separate Regional Councils for each area constituted as an autonomous region.

- In all, there are 10 areas in the Northeast that are registered as autonomous districts – three in Assam, Meghalaya and Mizoram and one in Tripura.

- These regions are named as district council of (name of district) and regional council of (name of region).

- Each autonomous district and regional council consist of not more than 30 members, of which four are nominated by the governor and the rest via elections, all of whom remain in power for a term of five years.

Back to the Basics: Special Status of Sixth Schedule Areas

- The Sixth Schedule was originally intended for the predominantly tribal areas (tribal population over 90%) of undivided Assam, which was categorised as “excluded areas” under the Government of India Act, 1935 and was under the direct control of the Governor.

- The Sixth Schedule of the Constitution provides for the administration of tribal areas in Assam, Meghalaya, Tripura and Mizoram to safeguard the rights of the tribal population in these states.

- In Assam, the hill districts of Dima Hasao, Karbi Anglong and West Karbi and the Bodo Territorial Region are under this provision.

- The Sixth Schedule provides for autonomy in the administration of these areas through Autonomous District Councils (ADCs) and the special provision is provided under Article 244(2) and Article 275(1) of the Constitution.

- The Governor is empowered to increase or decrease the areas or change the names of the autonomous districts. While executive powers of the Union extend in Scheduled areas with respect to their administration in fifth schedule, the sixth schedule areas remain within executive authority of the state.

-Source: Indian Economy

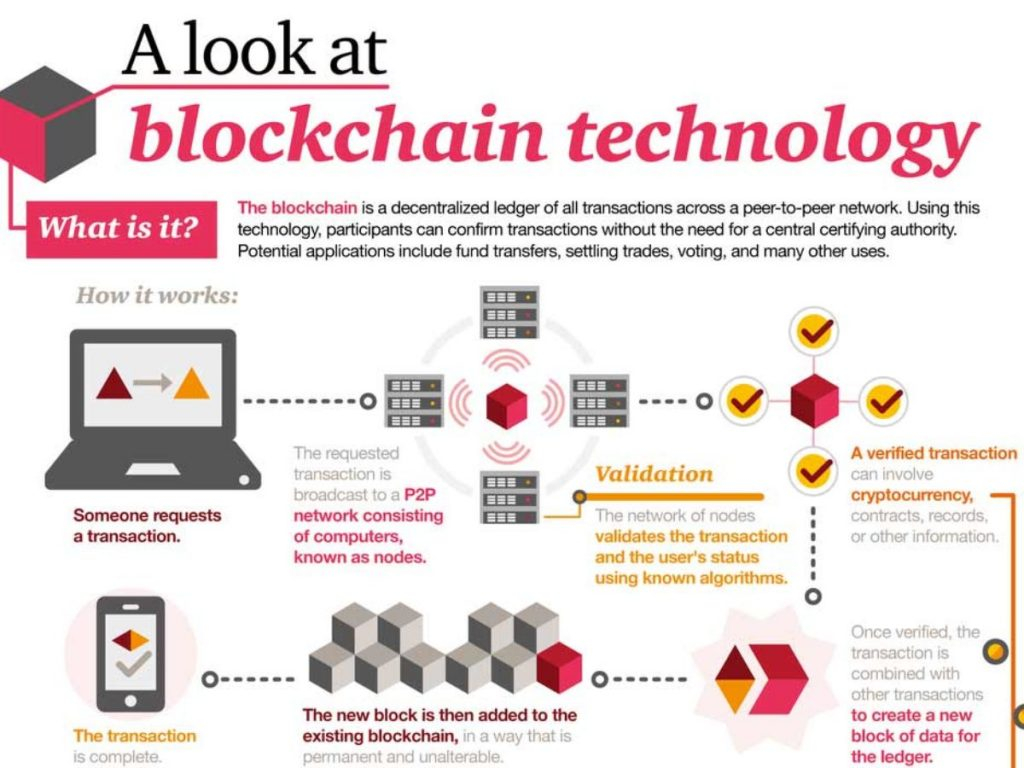

Crypto banking and decentralized finance

Context:

The development of Bitcoin and thousands of other cryptocurrencies in a little over a decade has changed the definition of money – due to which a parallel universe of alternative financial services has come into existence, allowing crypto businesses to move into traditional banking territory.

Relevance:

GS-III: Indian Economy (Banking, Money, Monetary Policy), GS-III: Science and Technology (Developments in Science and Technology, Application of Technology in Daily life, Blockchain technology)

Dimensions of the Article:

- What are cryptocurrencies?

- How are they different from actual currency?

- Alternative Services Offered by Cryptocurrencies

- About Decentralized Finance: An alternative finance ecosystem

What are cryptocurrencies?

- Cryptocurrencies are e-currencies that are based on decentralized technology and operate on a distributed public ledger called the blockchain.

- Blockchain records all transactions updated and held by currency holders.

- The technology allows people to make payments and store money digitally without having to use their names or a financial intermediary such as banks.

- Cryptocurrency units such as Bitcoin are created through a ‘mining’ process which involves using a computer to solve numerical problems that generate coins.

- Bitcoin was one of the first cryptocurrencies to be launched and was created in 2009.

How are they different from actual currency?

- The Main difference is that unlike actual currencies cryptocurrencies are not issued by Governments.

- Actual money is created or printed by the government which has a monopoly in terms of issuing currency. Central banks across the world issue paper notes and therefore create money and assign paper notes their value.

- Money created through this process derives its value via government fiat, which is why the paper currency is also called fiat currency.

- In the case of cryptocurrencies, the process of creating the currency is not monopolized as anyone can create it through the mining process.

How do cryptocurrencies derive their value?

- Any currency has its value if it can be exchanged for goods or services and if it is a store of value (it can maintain purchasing power over time).

- Cryptocurrencies, in contrast to fiat currencies, derive their value from exchanges.

- The extent of involvement of the community in terms of demand and supply of cryptocurrencies helps determine their value.

Alternative Services Offered by Cryptocurrencies

- Most notably, lending and borrowing are the primary kind of services offered by Cryptocurrencies.

- Investors can earn interest on their holdings of digital currencies – often a lot more than they could on cash deposits in a bank – or borrow with crypto as collateral to back a loan.

- However, it is important to note that Deposits are not guaranteed – along with which Cyberattacks, extreme market conditions, or other operational or technical difficulties could lead to a temporary or permanent halt on withdrawals or transfers.

About Decentralized Finance: An alternative finance ecosystem

- Decentralized finance, or DeFi, loosely describes an alternative finance ecosystem where consumers transfer, trade, borrow and lend cryptocurrency, theoretically independently of traditional financial institutions and the regulatory structures.

- The DeFi movement aims to “disintermediate” finance, using computer code to eliminate the need for trust and middlemen from transactions.

- DeFi platforms are structured to become independent from their developers and backers over time and to ultimately be governed by a community of users.

Benefits

- Innovators argue that crypto fosters financial inclusion. Consumers can earn unusually high returns on their holdings, unlike at banks.

- Crypto finance gives people long excluded by traditional institutions the opportunity to engage in transactions quickly, cheaply and without judgment. As crypto backs their loans, the services generally require no credit checks, although some take customer identity information for tax reporting and anti-fraud purposes. On a DeFi protocol, users’ personal identities are generally not shared, since they are judged solely by the value of their crypto.

-Source: Indian Economy

Sukhet Model: LPG cylinders in exchange for cow dung

Context:

An initiative called the Sukhet Model is being implemented in Bihar’s Madhubani district, which involves conferring LPG in exchange for cow dung and farmyard waste.

Relevance:

GS-III: Environment and Ecology (Environmental Pollution and Degradation, Conservation of Environment and Ecology)

Dimensions of the Article:

- About the Sukhet Model

- Benefits of the Sukhet Model

About the Sukhet Model

- The Sukhet Model was launched by the agricultural department as part of the climate resilient agricultural programme in 2019.

- It is an initiative by Dr. Rajendra Prasad Central Agriculture University (RPAU) in Sukhet village in Bihar’s Madhubani district, which allows women to get their LPG cylinders refilled every two months in exchange for cow dung and farmyard waste.

- Under Sukhet’s model, two local workers visit households that have cattle to collect dung and farmyard waste and bring it to a vermicomposting yard.

- A family has to provide 1200 kgs of cow dung and wet garbage waste every two months to get their LPG gas cylinders refilled for free. The family needs to meet the target of 20 kg of cow dung and garbage waste every day.

- The waste collected from the villages is used in manufacturing vermicompost, which is made available to farmers.

Benefits of the Sukhet Model

- The Sukhet Model ensures four-fold benefits:

- Ensures a pollution-free environment at home,

- Waste disposal,

- Monetary assistance for LPG cylinders, and

- Availability of organic fertilisers to the local farmers.

- The Villagers get good quality vermicompost which is cheaper than the market price.

- Implementing the Sukhet model in various districts of Bihar will also generate employment for the local youth and to make village soil nutrient self-sufficient.

- The program was lauded by Prime Minister Modi in one of his episodes of ‘Mann ki Baat’. He said that the implementation of Sukhet model in the village has brought ease to the household and has given strength to the Swachh Bharat Mission, besides providing benefits to the farmers.

-Source: The Hindu