Context:

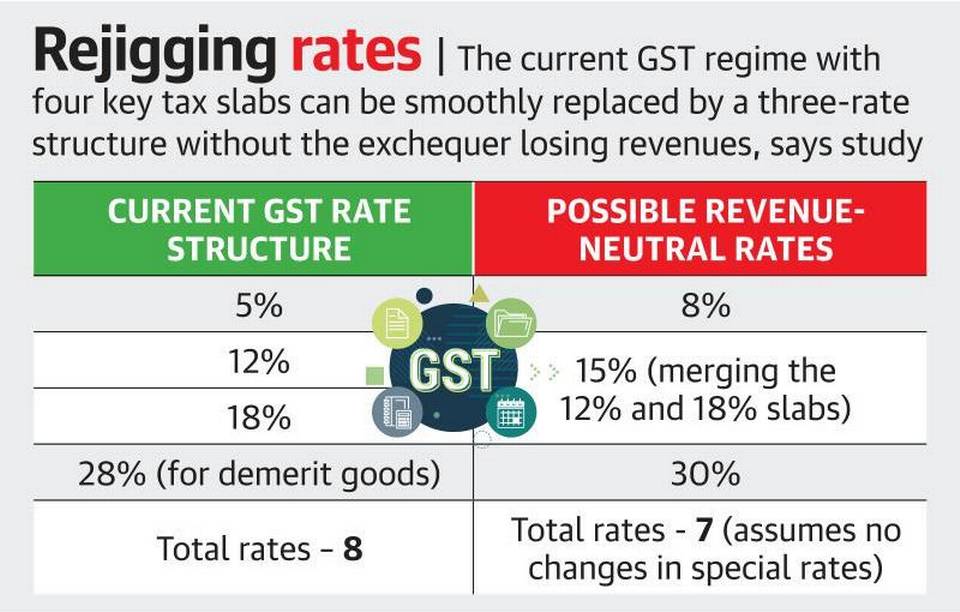

The Government can rationalise the GST rate structure without losing revenues by rejigging the four major rates of 5%, 12%, 18% and 28% with a three-rate framework of 8%, 15% and 30%, as per a National Institute of Public Finance and Policy (NIPFP) study.

Multiple rate changes since the introduction of the GST regime in July 2017 have brought the effective GST rate to 11.6% from the original revenue neutral rate of 15.5% according to the Finance Minister.

Relevance:

GS-II: Social Justice (Government Interventions and Policies, Issues arising out of the design and implementation of Government Policies)

Dimensions of the Article:

- GST and GST Council

- The findings of the NIPFP

- What are the key decisions made by GST Council?

About GST, GST Council

The findings of the NIPFP

The GST Council has tasked a Group of Ministers, headed by Karnataka CM Basavaraj S. Bommai, to propose a rationalisation of tax rates and a possible merger of different tax slabs by December to shore up revenues.

Understanding the numbers

- The findings of the NIPFP, an autonomous think tank backed by the Finance Ministry, show that merging the 12% and 18% GST rates into any tax rate lower than 18% may result in revenue loss.

- The NIPFP study proposes that the GST Council may consider a three-rate structure by adopting 8%, 15% and 30% for revenue neutrality.

- The nature of rate changes has also meant that over 40% of taxable turnover value now falls in the 18% tax slab, thus any move to dovetail that slab with a lower rate will trigger losses to the tax kitty that need to be offset by marginal hikes in other remaining major rates — 5% and 28%.

- The 28% rate is levied on demerit goods such as tobacco products, automobiles and aerated drinks, along with additional GST compensation cess.

- If the revenue loss from merging the 12% and 18% slabs were to be met by just hiking the rate on demerit or sin goods, the highest GST rate would have to be raised to almost 38%. Alternatively, the lowest standard rate will have to be raised from 5% to about 9%.

- Currently, the GST regime levies eight different rates, including zero for essential goods and special rates of 0.25% on diamonds, precious stones and 3% on gems and jewellery.

Conclusions of the study

- The NIPFP paper assumes these rates remain unchanged after noting that raising rates on ‘high-value low volume goods’ like precious stones and jewellery ‘may encourage unaccounted (undisclosed) transactions and therefore revenue leakages’.

- The results are indicative given the limitations of data, but the methodology developed in this paper could be useful for any future analysis of restructuring of the GST rate structure.

- The GST Council may consider placing some aggregate data in the public domain to help policy research as binding data limitations hinder meaningful research of the GST regime.

What are the key decisions made by GST Council?

- On Covid-19 Treatment: Existing concessional rates for Covid-19 medicines: Remdesivir (5 per cent), Tocilizumab (nil), Amphotericin B (nil), and anti-coagulants like Heparin (5 per cent) have been extended till December 2021. Along with this, a reduction of GST rate to 5 per cent on more Covid-19 treatment drugs like Itolizumab, Favipiravir etc., was also extended. However, the concessional tax for medical equipment will end on September 2021 as decided previously.

- On other medicines: The Council also decided to remove GST on the import of muscular atrophy drugs like Zolgensma and Viltepso, which cost crores of rupees. The GST rate for Keytruda, used for the treatment of cancer, has been cut to 5 per cent from 12 per cent.

- On Fortified rice: The Council also cut GST rates on fortified rice kernels to 5 per cent from 18 per cent.

- On Biodiesel: The Council also cut GST rates on bio-diesel for blending in diesel to 5 per cent from 12 per cent.

- On Ores and related: GST on ores and concentrates of metals such as iron, copper, aluminum, and zinc has been increased from 5 per cent to 18 per cent, and that on specified renewable energy devices and parts from 5 per cent to 12 per cent.

- On Packaging and other waste generating products: Cartons, boxes, bags, and packing containers of paper will now attract a uniform 18 per cent tax in place of the 12 per cent and 18 per cent rates. Waste and scrap of polyurethanes and other plastics will also see tax going up to 18 per cent from 5 per cent currently.

- On Soft-drinks: The rate for carbonated fruit beverages and carbonated beverages with fruit juice will attract a GST rate of 28 per cent, plus compensation cess of 12 per cent.

- On inclusion of fuel under GST: The Council discussed the issue only because the Kerala High Court had asked it, but felt it was not the right time to include petroleum products under GST.

- On inverted duty structure: The Council will also look at rate rationalisation under the inverted duty structure, and compliance measures through e-way bill and composition schemes. The Council has decided to set up a GoM to examine the issue of correction of inverted duty structure for major sectors; rationalise the rates and review exemptions from the point of view of revenue augmentation.

- Latest Decision On Compensation cess mechanism

- The Council also decided to put an end date of June 2022 to the compensation mechanism, as mandated in law.

- The levy of compensation cess will continue from July 2022 onwards till March 2026 to service the borrowing, which had been resorted to in order to bridge the compensation gap in the years 2020-21 and 2021-22.

- The debt for making compensation payments to states is estimated to be around Rs 2.7 lakh crore.

- In the previous GST Council meeting, it had been decided that beyond July 2022, the collection of cess would be for “payment of loans taken”. Beyond July 2022, the cess that the government collecting, as agreed in the 43rd Council meeting, is for the purpose of repaying the loans given to states since 2020.

- Latest Decision On e-commerce operators

- Effective January 1 2022, the Council has decided to make e-commerce operators engaged in restaurant services liable for payment of tax. This will essentially shift the responsibility of paying the 5 per cent GST to the aggregators from the restaurants.

- As a result of this, the restaurants will also have to mandatorily register themselves as is done by e-commerce sellers.

-Source: The Hindu